LNG is used in numerous countries worldwide as a cleaner and more efficient substitute for conventional fossil fuels and is expected to play an instrumental role as the world transitions towards net-zero emissions.

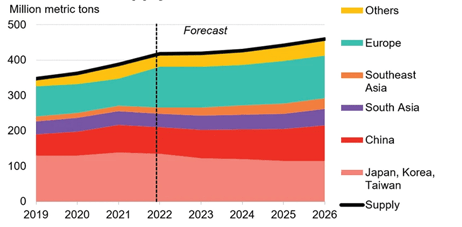

The world imported more LNG last year than ever before, up to 409 million tonnes from 387 million tonnes in 2021, according to data from Refinitiv. The record volume level came from new supply trains as well as increased demand fuelled by European countries’ rejection of Russian piped natural gas as a result of Russia’s incursion into Ukraine.

Europe’s push to replace Russian piped gas with LNG caused prices to hit record levels in 2022. In response, demand for LNG in Asia fell to 250 million tonnes in 2022, down from 270 million tonnes in 2021 as unaffordable prices stifled Asian demand. The largest drop was in China due to persistent COVID-related lockdowns, resulting in Japan reclaiming its spot as the world’s largest LNG importer.

In 2022, the United States and Qatar tied as the world’s top exporters of LNG, exporting 81.2 million tonnes according to ship-tracking data compiled by Bloomberg. The United States will need to continue building more LNG export capacity if it wants to hold onto the top spot through the end of this decade, which is supported by ample low-cost supplies of natural gas.

Qatar is in the midst of an enormous expansion to its production facility, which could solidify its position as the LNG leader from 2026. Australia is poised to remain as the world’s third-largest supplier.

Looking forward, there is support for the development of new liquefaction infrastructure from both the supply and demand sides. The demand for LNG is predicted to continue its upward trend. Investment in downstream LNG infrastructure is increasing globally, with more than 370 million tonnes of regasification capacity currently being developed. Moreover, it is expected that nine new markets will enter the LNG trade in the next two years, including Vietnam, the Philippines, and Ghana.

Global LNG supply and demand

Source: Bloomberg NEF April 2023

Decarbonisation

Clean energy investment has picked up in recent years but is still well short of the levels required to meet global targets. LNG can play a role in the global goal to decarbonise by serving as a transitional fuel to help reduce greenhouse gas emissions in certain sectors, such as electricity generation and transportation.

Compared to coal, LNG produces 40 per cent less carbon dioxide (CO2) when burned in power plants and 30 per cent less than oil, making it a cleaner-burning fuel. Additionally, LNG facilities can use carbon capture and storage (CCS) technology to capture and store carbon emissions, further reducing their carbon footprint.

However, it is important to note that while LNG is a cleaner alternative to coal and oil, it is still a fossil fuel and emits greenhouse gases. To achieve the global goal of decarbonisation, there needs to be a transition towards renewable energy sources, such as wind and solar.

Opportunities in infrastructure investment

From an essential infrastructure investment perspective, investors can access the global LNG market through owning energy infrastructure companies like Cheniere Energy (NYSE: LNG), Sempra Energy (NYSE: SRE), and Williams Companies (NYSE: WMB) in the United States.

Cheniere and Sempra both own and operate LNG export facilities in the United States, with capacity mostly secured under long-term contracts in which customers are generally required to pay a fixed fee with respect to the contracted volumes irrespective of whether the customer elects to take delivery of the cargoes or not.

Similarly, Williams owns and operates Transco, which is the backbone of the US natural gas pipeline network spanning 25 states, handling a third of the country’s natural gas production with take-or-pay agreements serving numerous LNG export facilities.

In Australia, gas producers like Woodside (ASX: WDS) and Santos (ASX: STO), while they do not qualify as essential infrastructure and are not held in our portfolio, they do own and operate LNG export facilities, which follow a different commercial model compared to their US counterparts. Typically, Australian producers own the entire value chain from the resource to midstream activities, pipelines, and export facilities.

This structure results in more direct exposure to commodity prices and demand and supply volatility, with Australian LNG pricing largely linked to the USD oil price with a corresponding slope, while US LNG exporters have fixed fee contracts. Consequently, Australia’s current commercial model for LNG export facilities does not align with our strict essential infrastructure criteria, particularly their commodity exposure which is volatile compared to the regulated and contracted exposure offered through energy infrastructure which is relatively hedged from commodity price risk.

The primary way to gain exposure to the LNG export thematic in Australia from an essential infrastructure perspective is through companies like APA Group (ASX: APA). APA owns the Wallumbilla Gladstone Pipeline, which connects Shell Energy’s natural gas fields in Queensland’s Surat Basin to the Queensland Curtis LNG export facility.

Looking at Europe, the Grain LNG import terminal operated by utility National Grid (LSE: NG) in the United Kingdom connects global supply of LNG to the European energy market and can also serve up to 20 per cent of the UK’s gas demand. Although it constitutes a minor portion of National Grid’s total operations, it is nevertheless a good example of how to gain exposure to the LNG thematic.

Minimising risks with managed fund investment

Of course, there are risks associated with LNG that can adversely impact infrastructure companies. While Ausbil’s definition of essential infrastructure focuses on regulated and contracted volumes to generate earnings and cashflows as a way to mitigate price and demand volatility, market sentiment can still have an impact. This means that even if the income streams remain relatively stable, listed infrastructure companies may still experience a decrease in trading due to perceptions about the direction of gas prices or the strength of demand.

Ausbil invests in a combination of quality, value, and ESG considerations. Short-term volatility can impact share prices but over the longer term, where we believe the fundamentals of a business remain unchanged, this can create a disconnect between the share price and fundamental value.

Investing in LNG is an exciting and growing area of opportunity in the listed infrastructure space. Demand is growing, there are significant barriers to entry and companies enjoy long-term contracts that secure cashflows for many years. By selecting the companies with the best assets, superior market position, and with the most secure long-term contracts, it can allow investors to tap into this long-term secular growth theme without taking on short-term commodity price risk.

Natasha Thomas, portfolio manager, energy & communications in Ausbil’s Global Essential Infrastructure team

{kind=link}