In its attempts to further prolong Australia’s record-breaking, 28-year economic expansion and because Australian inflation remains below its 2 per cent “target”, the RBA is now resorting to cutting interest rates to the bone. Many are even suggesting that the RBA may resort to quantitative easing at some stage to stimulate the Australian economy if the central bank’s continued rate cuts do not lead to a pick-up in economic growth and jobs in Australia.

The truth is that the RBA has joined the world’s central banks in conducting an experiment. Their paradigm is that the economy will benefit from policies based on economic theories that, in reality, have previously resulted in major imbalances and have frequently ended in crises: the technology boom and bust, the housing boom and mortgage financing bust in the US followed by a global financial crisis, and several other booms and busts such as those experienced in Iceland, Spain, and Ireland. The common theme in all these events is easy access to very cheap credit.

The intended effects of lower interest rates

Raising and lowering interest rates – the price of money – are popularly believed to stimulate or slow an economy and, in the short term, this is almost certainly true. In the longer term, however, a continual bias toward stimulating the economy in this manner often has the reverse effect in that imbalances and bubbles are eventually fostered and that the economic growth temporarily created proves unsustainable.

Lower interest rates clearly reduce mortgage repayments and, if consumers spend this interest savings, it will give the economy a short-term boost. The more important aspect of lowering interest rates is to greatly encourage the corporate sector to borrow more with the aim of expanding their enterprises by building new productive facilities – like new mines or factories – as this results in more jobs and sustained wealth creation in the longer term.

One of the many problems with most economic theories is that they assume you can adjust one factor and nothing else changes except what you intend to be affected by your adjustment. In isolation, lowering interest rates should encourage companies to use cheap debt to borrow to invest by building factories or to fund more investment in R&D and innovation with the aim of lifting the longer term productive capacity.

The unintended consequences

It is often said that interest rates are a very blunt tool and, in the real world, ultra-low interest rates can actually act counter to the intentions of what many central banks – including the RBA – seek to achieve. There are many unintended consequences of lower interest rates which we’ve seen play out in Europe and Japan and are now seeing in Australia. We’ve focused on three of these below.

1. Highly geared consumers are rewarded and long-term savers are penalised and encouraged to take on more risk when interest rates are extremely low

As with many central banks overseas, the RBA seems to take little account of the fact that they are sending the wrong message to society at large. By lowering interest rates, the RBA is making it cheaper for consumers to borrow and encouraging them to spend. Meanwhile, the same low rates are effectively penalising those who have saved all their lives in the hope of living in retirement off the interest earnt from their savings.

Households with high borrowings may have more disposable income as the cost of servicing debt declines, and this can lead to more consumption, which increases GDP in the short term. However, over the long term, it does nothing to lift the growth rate of the economy – in fact one can argue it takes away from future economic growth as consumers could end up being more highly geared going forward if it leads to a surge in spending.

This interest saving by borrowers is at least partially offset by the negative effect on savers and retirees, whose spending power is actually lowered.

On the other hand savers have been driven to look beyond the safe options of bank accounts and term deposits – which are offering very low returns. As of October 2019, one-year term deposit rates are at 1.6 per cent. Effectively, to earn $20 (before tax) a day in interest – which will hardly afford the holder a lavish lifestyle – you now need to have over $500,000 on term deposit.

As these savers seek higher return alternatives, they are pushed up the risk curve and existing asset prices are pushed higher. Sharemarkets around the world have benefited as savers venture into stocks. Alternative investments and even speculative assets like cryptocurrencies, art and classic cars have also appreciated.

Higher prices for houses, shares and other assets benefit asset owners but penalise people who don’t own assets. People who do not yet own a home struggle to buy one when prices are many times disposable income as they are in Australia. In favouring debtors over savers and asset owners over people without assets, central banks are effectively redistributing income and widening the gap between the haves and the have nots.

As the prices of many financial assets have already soared, people are being incentivised to continue to buy these assets. For many people in or approaching retirement, this is not the best time to be taking on more risk as a significant decline in the value of these risky assets could severely impact their ability to fund their own retirement.

The rise in inequality is surely not part of any master plan of central banks. Inequality could well be behind the rise in populist and nationalist political candidates and parties that we have seen in many countries in the developed world.

2. Lower interest rates do not appear to be leading to many companies expanding their productive capacity but are boosting asset prices instead

Companies may borrow more because the cost of borrowing is lower, but instead of investing in new assets such as factories and innovation – which will spur long-term economic growth because of the extra jobs created – many are using these borrowed funds to buy existing assets.

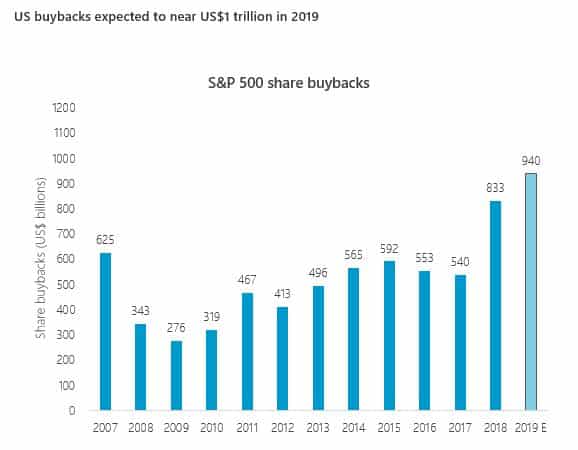

This is most clearly seen in the amount of share buybacks undertaken by US-listed corporations in the last few years. As seen in the chart below, buybacks in 2019 are expected to reach almost US$1 trillion in 2019, with the average leverage of most US companies increasing over the last few years as a consequence.

It makes sense for a company to make share buybacks when it has an undergeared balance sheet and few expansion opportunities. However, it appears that the current management of many US companies is taking advantage of low interest rates today to buy back their own shares.

In the short term, this enhances earnings per share, a measure often tied to their incentive payments. However, in the long term, this approach may well impede growth as future management teams have to use future cashflows to pay down the debt being accumulated today.

3. Ultra-low interest rates do not necessarily lead to higher inflation or a healthier corporate sector

The capitalist system is based on competitive markets fostering an efficient allocation of scarce resources.

By artificially controlling the price of money or the interest rate, funding is not necessarily scarce, and companies or entrepreneurs can set up in competition with well-funded companies without having a sensible or economic business model. While innovative competition deserves success, businesses that cannot make money and pay interest and repay debt should naturally fail.

It can clearly be seen that ultra-low interest rates for a sustained period of time – as seen in Japan – actually support many overgeared, old and inefficient companies as, when debt is so cheap, many of these companies do not fail as they should.

Unsound companies, or “zombie companies”, survive and create competition for sounder healthier companies that don’t rely on almost free funding to survive. This has had the impact of actually lowering prices and therefore, inflation, in some economies such as Japan – which is contrary to what the RBA is seeking to achieve.

We may also see this in some sectors of the Australian economy where more highly geared, weaker and, often, unsustainable competitors stay afloat in areas such as petrol retailing and the telecommunications industry. This is often pushing prices lower and reducing inflation.

In addition, when these companies funded by cheap debt are setting up in competition with more established companies, the incumbents are forced to try and maintain margins by keeping wages growth low or retrenching labour in order to compete with unsustainable start-ups.

Many companies have grown to significant size without ever turning a profit, generating free cash flow or providing a return on capital to justify their funding. An example is Uber: while consumers appreciate the choice and the lower transportation fares around the world, the fact that Uber cannot make money even though it has reached scale is an indictment of its business model.

Conclusion

When you consider all the likely effects of very low interest rates, you can see that very few are positive for the economy in the long term, and the true net benefit to the economy is far from certain. What can be said with certainty is that it is leading to a redistribution of income and wealth (between individuals and between businesses) which we do not believe was ever the intended objective of central banks around the world – including the RBA.

Surely the RBA should consider the obvious evidence of the recent past in places like Europe and Japan. As Einstein is credited with saying: “The definition of insanity is doing the same thing over and over again and expecting different results.” We have had decades of money and credit growing much faster than output. Inflation has trended down. Growth in output has trended down as interest rates, set by the government’s responsible authorities that we know as central banks, have trended down.

Economic theory would suggest that if money growth exceeds output growth than there will be inflation (Milton Friedman). This has been true, but the inflation has been concentrated in asset prices and not in goods and services prices that are measured by the consumer price index (CPI). Interest rate cuts have increased money and credit, but nearly all of the inflation we have seen has been asset price inflation while economic growth continues to trend down.

Faced with such evidence why do investment banks, mainstream economists and the media applaud interest rate cuts? If a house is bought and then sold for a higher price, has any real value been created? It’s the same house. The higher price just means a devaluation of the unit of measurement, the local currency. If low interest rates and ease of borrowing were the foundation of strong growth, surely Japan and Europe would be now be growing very strongly. Instead we see that people in Europe, faced with such paltry returns on their savings, are saving more to try and achieve some sort of return to live comfortably in their retirement.

For years economic policy has been geared (no pun intended) towards short-term fixes. Monetary policy simplistically says that lower interest rates will boost consumption and investment, ignoring historical evidence and all the other inconvenient consequences like social inequality. In the context of record levels of debt, central banks stubbornly persist in trying to force highly geared households to take on yet more debt, or companies that may have sensible balance sheets to take on leverage that may be inappropriately high. At some point, the debt will have to be repaid or will have to be written off in a crisis, with losses inevitably borne at least in part by everyone.

Anton Tagliaferro, investment director and Hugh Giddy, senior portfolio manager, Investors Mutual Ltd (IML)

{kind=link}