From late-2012 to mid-2015, markets were fairly stable and resilient. Simply going long in the market was amply rewarded at relatively low risk.

In this resilient state, we see evidence of the trade-off that is taught in capital markets classes and that is pervasive in financial literature: risk is generally rewarded with return. However, the risk environment that accompanies periods of low returns is generally not as well behaved.

In a post-Brexit world, the economic landscape appears to have changed, as there is evidence that we have returned to a more fragile investment environment.

We see global uncertainties rising and wider dispersion of expected fiscal and monetary outcomes across the globe, which we believe to be key drivers behind this shift.

In these fragile markets, we expect to see three main characteristics:

1) Market volatility will be higher than average and unstable;

2) Extreme events, both positive and negative, will be more frequent; and

3) Market risk (beta) will not necessarily be rewarded with return.

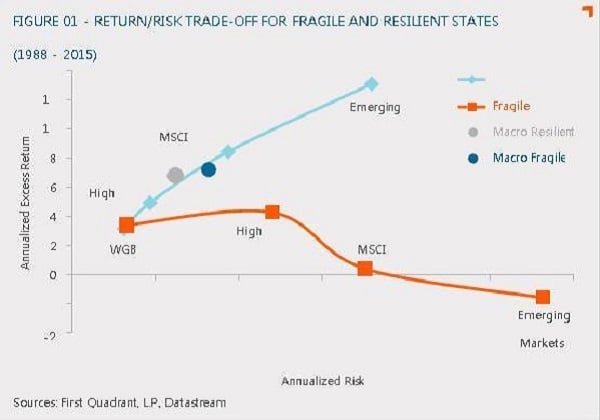

Fragile markets, as you can see, paint a markedly different picture from the characteristics of resilient markets. Risk is significantly higher for equities and high-yield bonds, while returns are quite low.

The relationship between risk and return seems largely random, and these fragile markets appear more often than you may think, as they encompassed 167 months of the total 312 months starting January 1990. (See fig 1)

So, how should investors structure their portfolios and mandates in periods of fragile markets? What sort of investment mindset is needed during fragile times?

We make the following observations and suggest a few investment considerations, but in short, the key is adaptability.

In cases where a super fund’s portfolio cannot adapt quickly because the process of reallocating assets takes time, it may become important that at least some of the underlying managers be adaptable.

Incorporate top-down orientation

Diverging growth and monetary policy across the globe lead to dislocations and thus more opportunity for strategies with a macro framework. Rising interest rates in the US versus negative interest rates in certain other developed economies is one example of this type of divergence.

Such an environment allows for directional positioning in some areas, and relative positioning in others. Idiosyncratic bets on political events such as Brexit are also fair game for macro investors.

Liquid investments are key to profiting from these conditions since investors need to be nimble; derivatives, such as equity futures and currency forwards, are typically used in these types of macro programs.

Currencies may also be also a prime source of uncorrelated return, since many macro events are reflected first in the underlying currencies of the markets in question.

Bets on political events such as Brexit, for example, can be made exclusively in liquid currency forward markets.

As for security selection, incorporating top-down views along with bottom-up analysis can become critical as securities react increasingly to macro events and less to their underlying fundamentals.

Increase active share and seek out uncorrelated returns

Don’t abandon long only, broad market, total return strategies, but closely examine and think carefully about their structure and correlation to the overall portfolio, especially to equity markets.

Incorporating total return strategies that are designed to be uncorrelated to broad market betas may also be significant contributors. As market returns can be scarce, consider loosening constraints and guidelines to allow for increased potential.

If you’re passive, go active; if you’re long only, opt for 130/30 or long/short; look for capital-efficient ways to introduce more diversifying elements into the portfolio using “portable alpha” programs.

Note, however, it is important to check that the return stream is indeed “orthogonal” to underlying market exposures, and not merely beta disguised as alpha.

If you’re a taxable investor, tax-efficient strategies become crucial in a low-return environment whether uncertainty is high or low.

Fragile markets also present an attractive time to be more tactical, there are strong runs both up and down which can last for some time, though, in the end, the cumulative return will be low.

From 2008-2012, the MSCI World Index was down 7.3 per cent. However, this included a -48.1 per cent plunge from January 2008 to February 2009, and then a 78.8 per cent rebound from March 2009 to December 2012.

Beware of the difference between “buying on the dips” and “catching a falling knife.” It’s this distinction which makes tactical trading of trends difficult, though they can be rewarding.

Consider hedging and contrarian strategies

Tail-risk mitigation strategies, particularly with options, may be appropriate across the market cycle, but particularly in fragile markets – even though option prices increase due to higher volatility.

During the resilient phase of the cycle, option prices are low (due to low volatility) and primarily hedge against exogenous shocks – like the 1991 Russian coup – which are generally short-lived during this phase.

Tail-risk hedging can also smooth return streams during market corrections. But the fragile market environment has a high frequency of endogenous, large-tail events and extended long draw-downs.

With this in mind, it’s important for investors to either maintain their tail-risk hedging programs or start them despite the increased cost of options.

If you are still concerned about cost, dynamic tail-risk hedging strategies or proxy hedging through currency or bond investments may be rational.

Global market regions, asset classes and instruments that are being ignored presently may also provide another avenue to harness returns. Emerging markets and commodities are two such areas.

Conversely, stay away from overly crowded trades and assets. If you think the crowd is always wrong, then periods of high uncertainty tend to be the best times to be a contrarian since that’s when investors often make mistakes.

In summary, fragile market states are typically the most difficult for investors and require the flexibility to quickly adapt to changing market conditions. Those who don’t adapt will likely be left behind.

Ed Peters is First Quadrant LP’s partner, investments.

{kind=link}