In the world of investing, reducing risk without significant sacrifice is a rare opportunity.

However, within the fixed income space, there’s a chance to reduce risk in investor portfolios. While reducing risk is typically associated with lower returns, the opportunity to reduce interest rate risk, by switching some exposure from fixed rate to floating rate assets, may actually lead to improved returns, depending on the market environment and other factors such as bond market volatility.

This is particularly relevant in today’s fixed income landscape, where there’s extensive speculation about whether bond yields and interest rates have peaked. There’s no question that the direction of interest rates significantly affects the performance of bonds on the “fixed rate” side of fixed income investments. But what may often be overlooked is that changing interest rates have a far less direct impact on the price of assets on the “floating rate” side of the fixed income universe.

That’s because floating rate notes reset their coupon rates generally every 90 days, while fixed rate bonds price do not reset their coupons. It’s as if floating rate notes can “change their clothing” to suit the weather and are therefore less exposed to extreme conditions.

There are two important points to note when comparing fixed versus floating rate notes:

- Despite the naming convention of “fixed income”, the asset class can often include both fixed rate and floating rate choices from the same debt issuer.

- While the relationship between interest rates and fixed income returns can be beneficial when rates decline, it can also introduce significant volatility, especially with traditional bond funds as they often tend to have meaningful interest rate exposure.

Allocating to a fixed income strategy with floating rate assets rather than fixed rate assets can mitigate this risk. Although both floating and fixed rate bonds fall under the “fixed income” category, they can yield vastly different results when interest rates and bond yields fluctuate, even if they share the same issuer.

This can matter to the investor because timing the precise peak in interest rates is a challenging task and even experts can make errors in their predictions. To illustrate the importance of making the right fixed income allocations between fixed and floating, consider the example of two bonds issued by ANZ, one fixed and one floating.

ANZ example: Fixed and floating bond

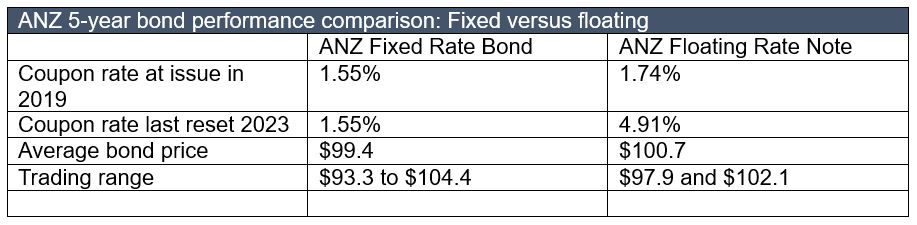

In August 2019, ANZ issued a fixed rate five-year senior bond with a $450 million face value and a coupon of 1.55 per cent. In the same period, they issued a floating rate security with a face value of $1.35 billion, which was identical to the fixed rate bond in every aspect except for its floating rate coupon. The floating rate bond’s coupon was initially set at 1.74 per cent (3M BBSW+77 bps) and adjusted every 90 days, reaching 4.91 per cent at its last reset. Both securities were issued at par, priced at $100.00.

The difference in performance between these two bonds becomes evident when you consider the inverse relationship between yields and fixed rate bond prices. As yields rise, fixed rate bond prices fall, and vice versa. With inflation on the rise, the RBA increased rates by 400 basis points between May 2022 and June 2023 to 4.10 per cent. While they’ve paused rate hikes since June, the risk of further increases remains due to persistent inflation. Bond yields have generally followed cash rates upward.

The fixed rate ANZ security pays a constant coupon, which is relatively low. As interest rates have been on the rise, the bond’s capital price has fallen. Since the end of 2019, the fixed rate bond has traded in a range of $93.3 to $104.4, with an average price of $99.4. It has traded at a discount to par 51 per cent of the time.

In contrast, the floating rate note’s coupon resets every 90 days, allowing it to rise with increasing interest rates. Consequently, the capital price has traded in a narrower range, fluctuating between $97.9 and $102.1, spending only 5 per cent of the time at a discount to par and averaging $100.7.

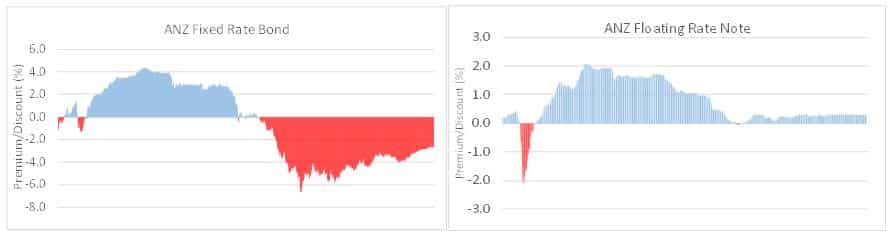

The trading ranges between the fixed and floating versions of the same bond can be illustrated in the charts below. The blue area highlights when the bond is trading at a premium to face value ($100) while the red shows when the bond is trading at a discount. The floating rate note in this period has experienced more time in the premium zone. Of course, this can change when interest rates are falling, but the point here is the volatility can be reduced with floating rate exposure.

The upshot is to be wary of increasing allocations to duration risk (fixed rate bonds) as there is doubts around the end of the cycle, and the cost of being wrong hurts. Floating rate notes can be an alternative, providing capital stability and sustainable and relatively low risk income flow.

Scott Rundell, chief investment officer, Mutual Limited

{kind=link}